2024 Year-End Stockholder Letter

2024 Year-End Stockholder Letter

February 12, 2025

Dear BREIT Stockholder,

Eight years ago, we designed BREIT to be a core portfolio holding that would provide diversification and build long-term wealth across market cycles. BREIT has delivered an annualized net return of +9.5% since inception (Class I), ~65% higher than publicly traded REITs and 2.7x private real estate.1,2 In 2024, 96% of BREIT’s distribution was classified as return of capital, bringing our 4.8% pre-tax Class I distribution rate to 7.5% on a tax-equivalent basis.3,4*

2024 in Review

At the beginning of 2024, we saw that values in our key sectors were bottoming and the pillars of an emerging real estate recovery were starting to take shape.5 However, significant interest rate volatility through much of the year, combined with a sharp increase in the 10-Year Treasury yield to 4.6% at year-end, impacted performance.6 Specifically, higher rates drove higher cap rates (lower valuation multiples), which reduced BREIT’s 2024 performance by 600bps and resulted in a Class I net return of +2.0%.7,8 Importantly, despite this headwind, real estate fundamentals in our core sectors remain healthy. BREIT’s portfolio generated 4% estimated cash flow growth, and our data centers were a powerful engine for growth.9** Furthermore, our valuations reflect today’s higher rate environment, setting us up for healthier go-forward performance.10

Strong long-term performance and resilience through volatility.

What’s in Store for 2025

We believe real estate values have now passed the cyclical bottom, though we are not expecting a V-shaped recovery.5 The U.S. economy remains resilient and we see continued strength in cash flow growth, supported by attractive supply and demand fundamentals. Unlike the post-GFC recovery which was driven by low interest rates amidst a weaker economy and anemic cash flow growth, we are seeing strong cash flow growth drive values higher, even as rates remain modestly elevated today.9, 11

Looking under the hood of BREIT’s portfolio, our key sectors are benefiting from long-term tailwinds such as outsized population growth in the Sunbelt, continued demand for e-commerce and the explosive growth in data and migration to the cloud.12,13 The supply picture for multifamily and industrial is equally favorable with new construction starts down two thirds from 2022 levels to near 10-year lows.14,15 To the extent that rates remain at these higher levels, this should constrain new supply further and correlate to a strong economy, supporting a multi-year period of strong cash flow growth.

We are also seeing healing in the capital markets, which is typically the first sign of a broader real estate recovery. Borrowing spreads have declined meaningfully, driving the all-in cost of capital down ~37% from the 2023 peak, and the availability of debt capital has increased significantly, with CMBS issuance up ~3x year-over-year.16,17 This is important because a healthy debt market is a critical driver of the broader real estate market.

Throughout 30+ years of investing at Blackstone, we have learned that you can’t wait for the all-clear signal to deploy capital. Blackstone Real Estate invested heavily into the GFC which produced one of the best vintages of performance.18 We didn’t wait then, and we aren’t waiting now: Blackstone Real Estate has deployed $28B globally in the last 12 months at historically attractive prices below replacement cost, underscoring our conviction in this recovery.19

BREIT Uniquely Positioned to Win20

Against this backdrop, we believe BREIT is exceptionally well-positioned. Our portfolio is ~90% concentrated in rental housing, industrial and data centers, our highest conviction sectors where we continue to see the strongest fundamentals. BREIT is ~70% concentrated in fast-growing Sunbelt markets with higher population, job and wage growth than the rest of the U.S.12 In each of our key sectors, BREIT benefits from market-leading platforms that provide data, operational expertise and boots on the ground to drive performance.21

Through active portfolio management, we continue to lean into the highest growth sectors such as data centers where we have increased exposure through our QTS platform from 1% in 2020 to 13% today.22 This has been a huge win for BREIT investors with data centers alone contributing ~500bps to BREIT’s performance in the last year.23 Since we acquired QTS in 2021, this investment has already generated significant implied profit, and we believe we are still in the early innings of growth.24*** We do not build data centers without a signed lease, and QTS’ $25B development pipeline is 100% pre-leased to investment grade technology companies on 15+ year contracts at high profit margins.25**** QTS also owns land with access to critical power that could support another $80B+ of development.25 As AI models continue to make significant leaps in efficiency, we believe this should catalyze more usage and adoption, driving demand for data centers. In fact, amidst recent developments and press around the space, large technology companies such as Meta, Microsoft, Amazon and Google have announced plans to invest heavily in their digital infrastructure this year. We believe QTS’ land bank, access to power and ability to execute with speed positions us to capture outsized demand in the space.

Within rental housing, we own a diversified portfolio with exposure to multifamily, student housing, single family rental housing and affordable housing. While elevated new supply coming online has moderated multifamily rent growth over the last year, ~80% of BREIT’s multifamily markets are now at or past peak supply and new deliveries will continue to sharply decline.26 This combined with the fact that it is ~50% more expensive to own vs. rent all sets up a very favorable outlook.27

BREIT’s industrial portfolio continues to outperform given our concentration in last-mile locations in top markets like Chicago, Dallas and Atlanta. In the second half of 2024, the number of leases signed across our portfolio increased 25% year-over-year and today we are signing leases at 35% higher rents vs. expiring leases.28,29 Continued e-commerce growth and the onshoring of manufacturing should propel future demand despite tariffs that could impact global trade.30 This strong demand combined with collapsing new supply is expected to generate continued cash flow growth, particularly as market rents are 24% above BREIT’s in-place rents.31

Finally, it’s important to have the right starting point on valuations to see the benefit of a real estate recovery in performance. BREIT’s valuations have been updated in real-time to reflect today’s higher rates, and since December 2021, we have increased our exit cap rates (decreased valuation multiples) by 16% and discount rates by 15% in our key sectors.10 This adds to our conviction in the go-forward outlook and positions us to benefit as values increase.

BREIT Today and for the Long-Term

We believe now is when you want to be invested in private real estate and BREIT is the vehicle to be in. When you consider the broader investment landscape today, we believe real estate offers attractive relative value. The S&P 500 is trading near all-time highs and corporate bonds have rebounded sharply from their 2022 trough, whereas the real estate recovery is just getting started with values rebounding only modestly so far.5,32 With history as our guide, we know that private real estate has delivered ~2x higher returns in recoveries vs. all other periods, which we believe sets the stage for outsized return potential.33 Finally, as a core portfolio holding over the long-term, private real estate can offer diversification benefits, compounding returns and help lower overall portfolio volatility in any market environment. For eight years, BREIT has done just this for our investors, and we believe BREIT is poised to deliver strong long-term real estate performance as we look ahead.

We remain grateful for your confidence, partnership and support.

Highlights from BREIT’s Q4 Stockholder Event

Watch for key insights on the investment environment, the real estate recovery and BREIT’s strong positioning.

BREIT Highlights

9.5%

annualized net return for Class I since inception in January 20171

~65%

higher returns than publicly traded REITs total return since January 20172

96%

of 2024 distributions characterized as Return of Capital (ROC)3

A Core Portfolio Holding Today and for the Long-Term

Why is Now a Good Time for BREIT?

Private Real Estate Opportunity

Today

2x higher returns following slowdowns vs. all other periods33

Long-Term

Diversification benefits + compounding returns

2024 BREIT Highlights

* Rental Housing includes the following subsectors as a percent of real estate asset value: multifamily (21%, including senior housing, which accounts for <1%), student housing (10%), single family rental housing (9%, including manufactured housing, which accounts for 1%) and affordable housing (9%).

Key Portfolio Metrics

Performance Summary

Total Returns (% Net of Fees)1

| Share Class | 2024 | 3-Year | Annualized Inception to Date | |

|---|---|---|---|---|

| Class I | 2.0% | 3.2% | 9.5% | |

| Class D | (No Sales Load) (With Sales Load)42 | 1.7% 0.2% | 2.9% 2.4% | 9.2% 9.0% |

| Class S | (No Sales Load) (With Sales Load)42 | 1.1% -2.3% | 2.3% 1.2% | 8.5% 8.1% |

| Class T | (No Sales Load) (With Sales Load)42 | 1.1% -2.3% | 2.3% 1.1% | 8.7% 8.2% |

Annualized Distribution Rates3

4.8%

Class I

4.6%

Class D

3.9%

Class S

4.0%

Class T

Download BREIT’s 2024 Year-End Stockholder Letter

* Assumes that the investment in BREIT shares is not sold or redeemed. The tax-equivalent distribution rate would be up to 1.5% lower taking into account deferred capital gains tax that would be payable upon redemption. See notes 3 and 4 for more information.

** Cash flow growth refers to same property net operating income (“NOI”) growth. Reflects BREIT’s year-over-year preliminary estimated same property NOI growth for the year ended December 31, 2024. See “Important Disclosure Information–Preliminary Estimated Same Property NOI Growth”.

*** Refers to estimated increase in valuations.

**** Reflects QTS’ development pipeline at 100% ownership interest. As of December 31, 2024, BREIT’s ownership interest in QTS was ~34% and the QTS investment accounted for 12.3% of BREIT’s real estate asset value.

- Represents Class I shares. Please see above for 2024, 3-year and inception to date (“ITD”) net returns. Class D, Class S and Class T shares listed as (with sales load) reflect the returns after the maximum upfront selling commission and dealer manager fees. Returns shown reflect the percent change in the NAV per share from the beginning of the applicable period, plus the amount of any distribution per share declared in the period. All returns shown assume reinvestment of distributions pursuant to BREIT’s distribution reinvestment plan, are derived from unaudited financial information, and are net of all BREIT expenses, including general and administrative expenses, transaction-related expenses, management fees, performance participation allocation, and share class-specific fees, but exclude the impact of early repurchase deductions on the repurchase of shares that have been outstanding for less than one year. The inception dates for the Class I, D, S and T shares are January 1, 2017, May 1, 2017, January 1, 2017 and June 1, 2017, respectively. The returns have been prepared using unaudited data and valuations of the underlying investments in BREIT’s portfolio, which are estimates of fair value and form the basis for BREIT’s NAV. Valuations based upon unaudited reports from the underlying investments may be subject to later adjustments, may not correspond to realized value and may not accurately reflect the price at which assets could be liquidated. As return information is calculated based on NAV, return information presented will be impacted should the assumptions on which NAV was determined prove to be different. Past performance does not predict future returns. 2024, 3-year and ITD returns are annualized consistent with the IPA Practice Guideline 2018. Please see www.breit.com/performance for information on BREIT returns.

- Publicly traded REITs reflect the MSCI U.S. REIT Index total return. Private real estate reflects the preliminary NFI-ODCE net total return. BREIT’s Class I inception date is January 1, 2017. During the period from January 1, 2017 to December 31, 2024, BREIT Class I’s annualized total net return of 9.5% was ~65% higher than the MSCI U.S. REIT Index annualized total return of 5.7% and 2.7x the preliminary NFI-ODCE annualized total net return of 3.5%. BREIT does not trade on a national securities exchange, and therefore, is generally illiquid. The volatility and risk profile of the indices presented are likely to be materially different from that of BREIT including that BREIT’s fees and expenses may be higher and BREIT shares are significantly less liquid than publicly traded REITs. See “Important Disclosure Information–Index Definitions”.

- Reflects the current month’s Class I distribution annualized and divided by the prior month’s net asset value, which is inclusive of all fees and expenses. Annualized distribution rate for the other share classes: Class D 4.6%, Class S 3.9% and Class T 4.0%. Distributions are not guaranteed and may be funded from sources other than cash flow from operations, including, without limitation, borrowings, the sale of our assets, repayments of our real estate debt investments, ROC or offering proceeds, and advances or the deferral of fees and expenses. We have no limits on the amounts we may fund from such sources. As of September 30, 2024, 100% of inception to date distributions were funded from cash flows from operations. A portion of REIT ordinary income distributions may be tax deferred given the ability to characterize ordinary income as ROC. ROC distributions reduce the stockholder’s tax basis in the year the distribution is received, and generally defer taxes on that portion until the stockholder’s stock is sold via redemption. Upon redemption, the investor may be subject to higher capital gains taxes as a result of a lower cost basis due to the ROC distributions. Certain non-cash deductions, such as depreciation and amortization, lower the taxable income for REIT distributions. BREIT’s ROC in 2017, 2018, 2019, 2020, 2021, 2022, 2023 and 2024 was 66%, 97%, 90%, 100%, 92%, 94%, 85% and 96%, respectively. See “Important Disclosure Information” including “Tax Information”.

- 7.5% tax-equivalent distribution rate assumes that the investment in BREIT shares is not sold or redeemed and reflects the pre-tax distribution rate an investor would need to receive from a theoretical investment to match the 4.7% after-tax distribution rate earned by a BREIT Class I stockholder based on BREIT’s 2024 ROC of 96%, if the distributions from the theoretical investment (i) were classified as ordinary income subject to tax at the top marginal tax rate of 37%, (ii) did not benefit from the 20% tax rate deduction and (iii) were not classified as ROC. The ordinary income tax rate could change in the future. Tax-equivalent distribution rate for the other share classes are as follows: Class D: 7.2%; Class S: 6.1%; and Class T: 6.2%. The tax-equivalent distribution rate would be reduced by 1.5%, 1.4%, 1.2% and 1.2% for Class I, D, S and T shares, respectively, taking into account deferred capital gains tax that would be payable upon redemption. This assumes a one-year holding period and includes the impact of deferred capital gains tax incurred in connection with a redemption of BREIT shares. Upon redemption, an investor is assumed to be subject to tax on all prior ROC distributions at the current maximum capital gains rate of 20%. The capital gains rate could change in the future. At this time, the 20% rate deduction to individual tax rates on the ordinary income portion of distributions is set to expire on December 31, 2025. See “Important Disclosure Information–Tax Information” for more information.

- Green Street Advisors, as of December 31, 2024. Reflects the Commercial Property Price Index for All Property, which captures the prices at which U.S. commercial real estate transactions are currently being negotiated and contracted.

- U.S. Department of the Treasury, as of December 31, 2024.

- Refers to attribution of BREIT’s forward twelve-month cap rate movement for BREIT’s 2024 Class I returns, assuming no changes to any other factors impacting BREIT’s returns.

- Represents BREIT Class I shares. Please see above for 2024 net returns for other share classes.

- Cash flow growth refers to same property net operating income (“NOI”) growth. Reflects BREIT’s year-over-year preliminary estimated same property NOI growth for the year ended December 31, 2024. See “Important Disclosure Information–Preliminary Estimated Same Property NOI Growth”.

- Reflects Blackstone Proprietary Data. Exit cap rates reflects percent change in BREIT’s weighted average rental housing and industrial (BREIT’s two largest sectors, which accounted for 74% of real estate asset value) assumed exit cap rate for its real estate portfolio from December 31, 2021 to December 31, 2024, weighted by BREIT’s asset value in each sector for the respective time period. BREIT’s asset values are calculated monthly through a robust valuation process and include ground-up, asset-by-asset valuations that reflect real time inputs, allowing us to make dynamic adjustments as the market evolves. Discount rate reflects percent change in BREIT’s weighted average rental housing and industrial discount rate for its real estate portfolio from December 31, 2021 to December 31, 2024, weighted by BREIT’s asset value in each sector for the respective time period. Blackstone is the largest owner, buyer and seller of commercial real estate globally (Real Capital Analytics, as of December 31, 2024), which we believe provides BREIT with a significant data advantage and enables BREIT to adjust its valuations more rapidly to a changing market environment. Higher exit cap rates (equivalent to lower valuation multiples) and discount rates negatively impact the value of BREIT’s property investments. Exit cap rates and discount rates are key assumptions made by BREIT and utilized in the discounted cash flow methodology, which BREIT generally utilizes as the primary methodology to value properties. Exit cap rates and discount rates are assumptions used in BREIT’s monthly valuation process and are not a measure of future performance or return. BREIT discloses its NAV calculation, including discount rates and exit cap rates on a weighted average basis by sector, monthly in a prospectus supplement under the monthly NAV per Share section. See www.breit.com/prospectus. For further information, please also refer to the “Net Asset Value Calculation and Valuation Guidelines” in BREIT’s prospectus and periodic reports, which describe our valuation process and the independent third parties who assist us.

- GFC recovery interest rates reflects U.S. Department of the Treasury. Reflects the 10-Year U.S. Treasury Yield. Reflects the 2009-2012 daily average rate. Cash flow growth refers to same property net operating income (“NOI”) growth. Cash flow growth during the GFC reflects Citi data and represents weighted average quarterly same property NOI growth for equity REITs from 2009-2012.

- “Property Sector” weighting is measured as the asset value of real estate investments for each sector category divided by the asset value of all of BREIT’s real estate investments, excluding the value of any third-party interests in such real estate investments. Rental housing includes the following subsectors: multifamily (21%, including senior housing, which accounts for <1%), student housing (10%), single family rental housing (9%, including manufactured housing, which accounts for 1%) and affordable housing (9%). Please see the prospectus for more information on BREIT’s investments. “Region Concentration” represents regions as defined by the National Council of Real Estate Investment Fiduciaries (“NCREIF”) and the weighting is measured as the asset value of real estate properties for each regional category divided by the asset value of all of BREIT’s real estate properties, excluding the value of any third-party interests in such real estate properties. “Sunbelt” reflects the South and West regions as defined by NCREIF. “Non-U.S.” reflects investments in Europe and Canada. Our portfolio is currently concentrated in certain industries and geographies, and, as a consequence, our aggregate return may be substantially affected by adverse economic or business conditions affecting that particular type of asset or geography. “Fast-growing” reflects comparison between the South and West regions (“Sunbelt”) versus the rest of the United States as defined by NCREIF. Population growth reflects U.S. Bureau of Economic Analysis, as of September 30, 2024. Represents 5-year compound annual growth rate of population from mid-quarter Q3 2019 to mid-quarter Q3 2024. Job growth reflects U.S. Bureau of Labor Statistics data as of September 30, 2024. Represents 5-year compound annual growth rate of seasonally adjusted employees on nonfarm payrolls from September 2019 to September 2024. Higher wage growth reflects U.S. Bureau of Labor Statistics, as of June 30, 2024. Represents 5-year compound annual growth rate of employment-weighted average weekly wages from Q2 2019 to Q2 2024. While BREIT generally seeks to acquire real estate properties located in growth markets, certain properties may not be located in such markets. Although a market may be a growth market as of the date of the publication of this material, demographics and trends may change and investors are cautioned on relying upon the data presented as there is no guarantee that historical trends will continue or that BREIT could benefit from such trends.

- Growth in data refers to datacenterhawk, as of December 31, 2024. Reflects U.S. gross data center absorption in 2024 vs. 2019. Growth in e-commerce refers to Mastercard SpendingPulse, as of November 30, 2024. Reflects year-over-year sales.

- Multifamily reflects RealPage Market Analytics data, as of December 31, 2024. Represents annual starts as a percent of prior year end stock figures. Data reflects institutional-quality product across RealPage Market Analytics Top 150-tracked markets. Multifamily starts are distinct from U.S. Census completions (which have recently been elevated), starts and permits and total housing supply (which include both single family and multifamily), which may differ in volume over a given period. As of December 31, 2024, the multifamily (including senior housing) and affordable housing sectors accounted for 21% and 9% of BREIT’s real estate asset value, respectively.

- Industrial reflects CoStar data, as of January 15, 2025. Represents annual starts as a percent of prior year-end stock figures. As of December 31, 2024, the industrial sector accounted for 25% of BREIT’s real estate asset value.

- Blackstone Proprietary Data, as of January 3, 2025. Refers to decreasing all-in cost of capital and increasing availability of debt. All-in cost of capital reflects Blackstone Proprietary Data, as of January 3, 2025, and represents estimated all-in borrowing costs for high-quality logistics portfolio transactions. Base rate reflects 3-year SOFR swap rate (’23 wide as of October 18, 2023, and today as of January 3, 2025). Spread reflects weighted average spread across all rating tranches applied to estimated rating agency capital structures from each respective period. There can be no assurance that financing costs will continue to decline and changes in this measure may have a negative impact on our performance.

- Green Street Advisors, as of January 24, 2025. Represents total U.S. CMBS issuance volume in 2024 compared to 2023.

- Refers to Blackstone Real Estate net returns for BREP VI, which invested from February 2007 through August 2011 and produced a 2.5x MOIC.

- These transactions were made by Blackstone Real Estate, BREIT’s sponsor, and may not be representative of future acquisitions or dispositions or BREIT’s portfolio holdings. Blackstone Inc. is a premier global investment manager. The real estate group of Blackstone, Blackstone Real Estate, is our sponsor and an affiliate of our Adviser. Information regarding Blackstone and Blackstone Real Estate is included to provide information regarding the experience of our sponsor and its affiliates. An investment in BREIT is not an investment in our sponsor or Blackstone as BREIT is a separate and distinct legal entity. $28B refers to equity deployed and committed by Blackstone Real Estate for the twelve-month period ended December 31, 2024.

- “Win” refers to generating strong performance.

- “Market-leading platforms” refer to QTS, American Campus Communities and Link. As of December 31, 2024, BREIT’s ownership interest in QTS was ~34% and the QTS investment accounted for 12.3% of BREIT’s real estate asset value. As of December 31, 2024, BREIT’s ownership in ACC was 69% and the ACC investment accounted for 7.5% of BREIT’s real asset value. As of September 30, 2024, BREIT’s U.S. industrial portfolio accounted for ~35% of Blackstone Real Estate’s U.S. industrial portfolio.

- “Highest growth sectors” reflects FTSE NAREIT Equity REITs data and represents annualized performance of publicly traded residential, industrial and data center REITs since BREIT’s inception compared to other major REIT sectors. 2020 refers to BREIT’s real estate portfolio as of December 31, 2020.

- ~500bps refers to contribution to 1-Year BREIT Class I returns from the data centers, assuming no changes to any other factors impacting BREIT’s returns.

- Represents estimated appreciation in QTS values between acquisition date of August 31, 2021 and December 31, 2024, at 100% ownership and at BREIT’s share. Excludes income. Reflects estimated increase in total fair value of the QTS real estate investment and does not necessarily represent the price at which BREIT’s investments would sell. There can be no assurance that QTS would be able to realize this implied profit.

- As of December 31, 2024. $25B reflects total cost for committed development projects at 100% ownership. Reflects signed leases. There can be no assurance that these development projects will commence on their current expected terms, or at all, and this information should not be considered an indication of future performance. $80B+ reflects cost estimate of developing data center projects on existing land bank acres and excludes committed development projects, at 100% ownership. This information is provided to illustrate the potential for additional development projects at QTS’s existing land bank acres, and there can be no assurance that any development projects will arise at these land bank acres. In addition, future land bank opportunities could be allocated to other Blackstone vehicles instead of to QTS or BREIT.

- RealPage Market Analytics as of December 31, 2024. Reflects multifamily delivery forecast in BREIT’s U.S. multifamily markets. ~80% refers to the percentage of BREIT multifamily markets forecasted to be at or past peak supply by March 31, 2025.

- Blackstone Proprietary Data, as of January 13, 2025. Represents the difference between monthly cost of ownership (including mortgage payments, taxes, maintenance costs, insurance, and HOA fees) and monthly rents for Home Partners of America and Tricon portfolios. Cost of ownership assumes 30‐year fixed rate FHA mortgage, 3.5% amortized loan closing costs and 3.5% down payment.

- Reflects BREIT’s same-store industrial leasing volume growth from 2H’24 vs. 2H’23.

- As of December 31, 2024. Represents quarterly leasing spreads and compares new or renewal rents to prior rents or expiring rents, as applicable.

- Onshoring of manufacturing reflects Blackstone Proprietary Data, as of October 31, 2024.

- Blackstone Proprietary Data, as of December 31, 2024. Represents our estimate of the average embedded rent growth potential of BREIT’s industrial portfolio based on the difference between current in-place rents and current achievable market rents. See “Important Disclosure Information—Embedded Growth”. This is not a measure, or indicative, of overall portfolio performance or returns. Certain other BREIT property sectors have lower embedded rent growth potential. BREIT’s overall portfolio embedded growth potential was 11% as of December 31, 2024. BREIT’s industrial portfolio has a 3.6-year weighted average lease length. Reflects real estate properties only, including unconsolidated properties, and does not include real estate debt investments. For a complete list of BREIT’s real estate investments (excluding equity in public and private real estate-related companies), visit www.breit.com/properties. Embedded rent growth will not directly correlate with increased performance or returns and is presented for illustrative purposes only and does not constitute forecasts. There can be no assurance that any such results will actually be achieved. A number of factors, including operating expenses as described in BREIT’s Quarterly Report on Form 10-Q filed with the Securities and Exchange Commission on November 8, 2024, will impact BREIT’s net performance or returns. Any expectations that in-place rents have the potential to increase are based on certain assumptions that may not be correct and on certain variables that may change.

- S&P 500 reflects total gross return. Oct’22 Trough refers to October 12, 2022. Today refers to January 31, 2025. Corporate bonds reflect the total return of the Bloomberg U.S. Corporate High Yield Index. Sep’22 Trough refers to September 29, 2022. Today refers to January 31, 2025. Indices are meant to illustrate general market performance. Comparisons shown are for informational purposes only, do not represent specific investments and are not a portfolio allocation recommendation. See “Important Disclosure Information–Index Definitions”.

- NCREIF, as of June 30, 2024. Reflects the NFI-ODCE levered gross total returns during the 5-year recover periods post real estate (“RE”) downturns compared to the long-term average excluding 5-year recovery periods. Long-term average excluding 5-year recovery periods reflects annualized average 5-year returns from June 30, 1993 to June 30, 2024, excluding the 5 years following the Savings and Loan (“S&L”) Crisis (starting June 30, 1993) and Global Financial Crisis (“GFC”) (starting December 30, 2009). 5-year recovery periods post RE downturns reflect the average of annualized 5-year returns following the Savings and Loan Crisis and the Global Financial Crisis. Performance data shown represents the performance of an index and not that of BREIT. The NFI-ODCE index reflects total returns of various private real estate funds excluding management and advisory fees and should not be considered reflective of the performance of BREIT. See “Important Disclosure Information–Index Definitions” for more information.

- Reflects the 10-Year U.S. Treasury Yield. GFC Recovery reflects the 2009-2012 U.S. Department of the Treasury daily average rate. Today’s Recovery reflects the 10-Year U.S. Treasury Yield as of January 31, 2025.

- Cash flow growth refers to same property net operating income (“NOI”) growth. Cash flow growth during the GFC reflects Citi data and represents weighted average quarterly same property NOI growth for equity REITs from 2009-2012. Cash flow growth during Today’s Recovery reflects BREIT’s year-over-year preliminary estimated same property NOI growth for the year ended December 31, 2024. During the YTD period ended September 30, 2024 (latest period available), Citi data also reflected 4% weighted average quarterly same property NOI growth for equity REITs. See “Important Disclosure Information–Preliminary Estimated Same Property NOI Growth”.

- Total asset value is measured as (i) the asset value of real estate investments (based on fair value), excluding any third party interests in such real estate investments, plus (ii) the equity in our real estate debt investments measured at fair value (defined as the asset value of our real estate debt investments less the financing on such investments), but excluding any other assets (such as cash or any other cash equivalents). The total asset value would be higher if such amounts were included and the value of our real estate debt investments was not decreased by the financing on such investments. “Real estate investments” include wholly-owned property investments, BREIT’s share of property investments held through joint ventures and equity in public and private real estate related companies. “Real estate debt investments” include BREIT’s investments in commercial mortgage-backed securities, residential mortgage-backed securities, mortgage loans and other debt secured by real estate and real estate related assets, as described in BREIT’s prospectus. The Consolidated GAAP Balance Sheet included in our annual and interim financial statements reflects the loan collateral underlying certain of our real estate debt investments on a gross basis. These amounts are excluded from our real estate debt investments as they do not reflect our economic interest in such assets.

- Number of properties reflects real estate investments only, including unconsolidated properties, and does not include real estate debt investments. Single family rental homes are not reflected in the number of properties.

- Occupancy is an important real estate metric because it measures the utilization of properties in the portfolio. Occupancy is weighted by the total value of all consolidated real estate properties, excluding our hospitality investments, and any third-party interests in such properties. For our industrial, net lease, data centers, office and retail investments, occupancy includes all leased square footage as of the date indicated. For our multifamily, student housing and affordable housing investments, occupancy is defined as the percentage of actual rent divided by gross potential rent (defined as actual rent for occupied units and market rent for vacant units) for the three months ended on the date indicated. For our single family rental housing investments, the occupancy rate includes occupied homes for the month ended on the date indicated. For our self storage, manufactured housing and senior living investments, the occupancy rate includes occupied square footage, occupied sites and occupied units, respectively, as of the date indicated. The average occupancy rate for our hospitality investments was 73% for the twelve months ended September 30, 2024 and includes paid occupied rooms. Hospitality investments owned less than 12 months are excluded from the average occupancy rate calculation. Unconsolidated investments are excluded from occupancy rate calculations.

- Our leverage ratio is measured by dividing (i) consolidated property-level and entity-level debt net of cash and loan-related restricted cash, by (ii) the asset value of real estate investments (measured using the greater of fair market value and cost) plus the equity in our settled real estate debt investments. Indebtedness incurred (i) in connection with funding a deposit in advance of the closing of an investment or (ii) as other working capital advances will not be included as part of the calculation above. The leverage ratio would be higher if the indebtedness on our real estate debt investments and the pro rata share of debt within our unconsolidated investments were taken into account. The use of leverage involves a high degree of financial risk and may increase the exposure of the investments to adverse economic factors.

- Percentage fixed-rate financing is measured by dividing (i) the sum of our consolidated fixed-rate debt, secured financings on investments in real estate debt, and the outstanding notional principal amount of corporate and consolidated interest rate swaps, by (ii) total consolidated debt outstanding inclusive of secured financings on investments in real estate debt.

- Investment allocation is measured as the asset value of each investment category (real estate investments or real estate debt investments) divided by the total asset value of all investment categories, excluding the value of any third party interests in such assets.

- Assumes payment of the full upfront sales charge at initial subscription (1.5% for Class D shares; 3.5% for Class S and Class T shares). The sales charge for Class D shares became effective May 1, 2018.

Important Disclosure Information

Past performance does not predict future returns. Financial data is estimated and unaudited. All figures as of December 31, 2024 unless otherwise noted. Opinions expressed reflect the current opinions of BREIT as of the date appearing in the materials only and are based on BREIT’s opinions of the current market environment, which is subject to change. Certain information contained in the materials discusses general market activity, industry or sector trends, or other broad-based economic, market or political conditions and should not be construed as research or investment advice.

The properties, sectors and geographies referenced herein do not represent all BREIT investments. The selected investment examples presented or referred to herein may not be representative of all transactions of a given type or of investments generally and are intended to be illustrative of the types of investments that have been made or may be made by BREIT in employing its investment strategies. It should not be assumed that BREIT’s investment in the properties identified and discussed herein were or will be profitable or that BREIT will make equally successful or comparable investments in the future. Please refer to https://www.breit.com/properties for a complete list of real estate investments (excluding equity in public and private real estate related companies).

Blackstone Proprietary Data. Certain information and data provided herein is based on Blackstone proprietary knowledge and data. Portfolio companies may provide proprietary market data to Blackstone Inc. (“Blackstone”), including about local market supply and demand conditions, current market rents and operating expenses, capital expenditures and valuations for multiple assets. Such proprietary market data is used by Blackstone to evaluate market trends as well as to underwrite potential and existing investments. While Blackstone currently believes that such information is reliable for purposes used herein, it is subject to change, and reflects Blackstone’s opinion as to whether the amount, nature and quality of the data is sufficient for the applicable conclusion, and no representations are made as to the accuracy or completeness thereof.

Embedded Growth. Embedded growth represents Blackstone’s expectations for growth based on its view of the current market environment taking into account rents that are currently below market rates and therefore have the potential to increase. These expectations are based on certain assumptions that may not be correct and on certain variables that may change, are presented for illustrative purposes only and do not constitute forecasts. There can be no assurance that any such results will actually be achieved.

Logos. The logos presented herein were not selected based on performance of the applicable company or sponsor to which they pertain. In Blackstone’s opinion, the logos selected were generally the most applicable examples of the given thesis, theme or trend discussed on the relevant slide(s). All rights to the trademarks and/or logos presented herein belong to their respective owners and Blackstone’s use hereof does not imply an affiliation with, or endorsement by, the owners of these logos.

Preliminary Estimated Same Property NOI Growth. Represents BREIT’s preliminary estimated year to date same property NOI growth for the year ended December 31, 2024 compared to the prior year (based on the midpoint of the preliminary estimated range of same property NOI). This data is not a comprehensive statement of our financial results for the year ended December 31, 2024, and our actual results may differ materially from this preliminary estimated data. Net Operating Income (“NOI”) is a supplemental non-GAAP measure of our property operating results that we believe is meaningful because it enables management to evaluate the impact of occupancy, rents, leasing activity and other controllable property operating results at our real estate. We define NOI as operating revenues less operating expenses, which exclude (i) impairment of investments in real estate, (ii) depreciation and amortization, (iii) straight-line rental income and expense, (iv) amortization of above- and below-market lease intangibles, (v) amortization of accumulated unrealized gains on derivatives previously recognized in other comprehensive income, (vi) lease termination fees, (vii) property expenses not core to the operations of such properties, and (viii) other non-property related revenue and expense items such as (a) general and administrative expenses, (b) management fee paid to the Adviser, (c) performance participation allocation paid to the Special Limited Partner, (d) incentive compensation awards, (e) income (loss) from investments in real estate debt, (f) change in net assets of consolidated securitization vehicles, (g) income (loss) from interest rate derivatives, (h) net gain on dispositions of real estate, (i) interest expense, net, (j) loss on extinguishment of debt, (k) other income (expense), and (l) similar adjustments for NOI attributable to non-controlling interests and unconsolidated entities. We evaluate our consolidated results of operations on a same property basis, which allows us to analyze our property operating results excluding acquisitions and dispositions during the periods under comparison. Properties in our portfolio are considered same property if they were owned for the full periods presented, otherwise they are considered non-same property. Recently developed properties are not included in same property results until the properties have achieved stabilization for both full periods presented. We define stabilization for the property as the earlier of (i) achieving 90% occupancy, (ii) 12 months after receiving a certificate of occupancy, or (iii) for Data Centers 12 months after receiving a certificate of occupancy and greater than 50% of its critical IT capacity has been built. Certain assets are excluded from same property results and are considered non-same property, including (i) properties held-for-sale, (ii) properties that are being redeveloped, (iii) properties identified for future sale, and (iv) interests in unconsolidated entities under contract for sale with hard deposit or other factors ensuring the buyer’s performance. We do not consider our investments in the real estate debt segment or equity securities to be same property. For more information, please refer to BREIT’s Current Report on Form 8-K filed with the Securities and Exchange Commission on January 30, 2025 and the prospectus. Additionally, please see below for a reconciliation of preliminary estimated GAAP net income to preliminary estimated same property NOI for the years ended December 31, 2024 and 2023.

Select Images. The selected images of certain BREIT investments in this presentation are provided for illustrative purposes only, are not representative of all BREIT investments of a given property type and are not representative of BREIT’s entire portfolio. It should not be assumed that BREIT’s investment in the properties identified and discussed herein were or will be profitable. Please refer to www.breit.com/properties for a complete list of BREIT’s real estate investments (excluding equity in public and private real estate related companies), including BREIT’s ownership interest in such properties.

Tax Information. The tax information herein is provided for informational purposes only, is subject to material change, and should not be relied upon as a guarantee or prediction of tax effects. This material also does not constitute tax advice to, and should not be relied upon by, potential investors, who should consult their own tax advisors regarding the matters discussed herein and the tax consequences of an investment. A portion of REIT ordinary income distributions may be tax deferred given the ability to characterize ordinary income as Return of Capital (“ROC”). ROC distributions reduce the stockholder’s tax basis in the year the distribution is received, and generally defer taxes on that portion until the stockholder’s stock is sold via redemption. Upon redemption, the investor may be subject to higher capital gains taxes as a result of a lower cost basis due to the ROC distributions. Certain non-cash deductions, such as depreciation and amortization, lower the taxable income for REIT distributions. Investors should be aware that a REIT’s ROC percentage may vary significantly in a given year and, as a result, the impact of the tax law and any related advantage may vary significantly from year to year. At this time, the 20% rate deduction to individual tax rates on the ordinary income portion of distributions is set to expire on December 31, 2025. The tax benefits are not applicable to capital gain dividends or certain qualified dividend income and are only available for qualified REITs. If BREIT did not qualify as a REIT, the tax benefit would be unavailable. BREIT’s board also has the authority to revoke its REIT election. There may be adverse legislative or regulatory tax changes and other investments may offer tax advantages without the set expiration. An accelerated depreciation schedule does not guarantee a profitable return on investment and ROC reduces the basis of the investment. While we currently believe that the estimations and assumptions referenced herein are reasonable under the circumstances, there is no guarantee that the conditions upon which such assumptions are based will materialize or are otherwise applicable. This information does not constitute a forecast, and all assumptions herein are subject to uncertainties, changes and other risks, any of which may cause the relevant actual, financial and other results to be materially different from the results expressed or implied by the information presented herein. No assurance, representation or warranty is made by any person that any of the estimations herein will be achieved, and no recipient of this example should rely on such estimations. Investors may also be subject to net investment income taxes of 3.8% and/or state income tax in their state of residence which would lower the after-tax distribution rate received by the investor.

Third Party Information. Certain information contained in this material has been obtained from sources outside Blackstone, which in certain cases have not been updated through the date hereof. While such information is believed to be reliable for purposes used herein, no representations are made as to the accuracy or completeness thereof and none of Blackstone, its funds, nor any of their affiliates takes any responsibility for, and has not independently verified, any such information. This information involves a number of assumptions and limitations, and you are cautioned not to give undue weight to these estimates.

Trends. There can be no assurances that any of the trends described herein will continue or will not reverse. Past events and trends do not imply, predict or guarantee, and are not necessarily indicative of, future events or results.

Use of Leverage. BREIT uses and expects to continue to use leverage. If returns on such investment exceed the costs of borrowing, investor returns will be enhanced. However, if returns do not exceed the costs of borrowing, BREIT performance will be depressed. This includes the potential for BREIT to suffer greater losses than it otherwise would have. The effect of leverage is that any losses will be magnified. The use of leverage involves a high degree of financial risk and will increase BREIT’s exposure to adverse economic factors such as rising interest rates, downturns in the economy or deteriorations in the condition of BREIT’s investments. This leverage may also subject BREIT and its investments to restrictive financial and operating covenants, which may limit flexibility in responding to changing business and economic conditions. For example, leveraged entities may be subject to restrictions on making interest payments and other distributions.

Index Definitions

An investment in BREIT is not a direct investment in real estate, and has material differences from a direct investment in real estate, including those related to fees and expenses, liquidity and tax treatment. BREIT’s share price is subject to less volatility because its per share NAV is based on the value of real estate assets it owns and is not subject to market pricing forces as are the prices of the asset classes represented by the indices presented. Although BREIT’s share price is subject to less volatility, BREIT shares are significantly less liquid than these asset classes, and are not immune to fluctuations. Private real estate is not traded on an exchange and will have less liquidity and price transparency. The value of private real estate may fluctuate and may be worth less than was initially paid for it.

The volatility and risk profile of the indices presented is likely to be materially different from that of BREIT including those related to fees and expenses, liquidity, safety, and tax features. In addition, the indices employ different investment guidelines and criteria than BREIT; as a result, the holdings in BREIT may differ significantly from the holdings of the securities that comprise the indices. The indices are not subject to fees or expenses, are meant to illustrate general market performance and it may not be possible to invest in the indices. The performance of the indices has not been selected to represent an appropriate benchmark to compare to BREIT’s performance, but rather is disclosed to allow for comparison of BREIT’s performance to that of well-known and widely recognized indices. A summary of the investment guidelines for the indices presented is available upon request. In the case of equity indices, performance of the indices reflects the reinvestment of dividends.

BREIT does not trade on a national securities exchange, and therefore, is generally illiquid. Your ability to redeem shares in BREIT through BREIT’s share repurchase plan may be limited, and fees associated with the sale of these products can be higher than other asset classes. In some cases, periodic distributions may be subsidized by borrowed funds and include a return of investor principal. This is in contrast to the distributions investors receive from large corporate stocks that trade on national exchanges, which are typically derived solely from earnings. Investors typically seek income from distributions over a period of years. Upon liquidation, ROC may be more or less than the original investment depending on the value of assets. An investment in BREIT (i) differs from the Green Street Commercial Property Price Index in that such index represents various private real estate values with differing sector concentrations (ii) differs from high yield bonds and the Bloomberg U.S. Corporate High Yield Index in that private real estate investments are not fixed-rate debt instruments and such bonds represent debt issued by corporations across a variety of issuers with varying pricing, terms and conditions, (iii) differs from the MSCI U.S. REIT Index in that BREIT is not a publicly traded U.S. Equity REIT, (iv) differs from the NFI-ODCE in that such index represents various private real estate funds with differing terms and strategies, and (v) differs from equities and the S&P 500 Index in that private real estate investments are not large or mid cap stocks and are not publicly traded.

The Green Street Commercial Property Price Index (“CPPI”) is a value-weighted time series of unleveraged U.S. commercial property values with an inception date of December 31, 1997. CPPI is shown to illustrate general market trends for informational purposes only, does not represent any specific investment and does not reflect how BREIT has performed or will perform in the future. The index captures the prices at which commercial real estate transactions are currently being negotiated and contracted, measuring price changes across select property types covered by Green Street Advisors. All Property Sector weights: retail (20%), apartments (15%), health care (15%), industrial (12.5%), office (12.5%), lodging (7.5%), data center (5%), net lease (5%), self-storage (5%), and manufactured home park (2.5%). Apartments refers to multifamily, lodging refers to hospitality.

The Bloomberg U.S. Corporate High Yield Index is a broad-based benchmark that measures the USD-denominated, high yield, fixed rate corporate bond market. An investment in high-yield corporate bonds is generally considered to be a less risky investment than private real estate.

The MSCI U.S. REIT Index is a free float-adjusted market capitalization index that is comprised of equity REITs. The index is based on the MSCI USA Investable Market Index (IMI), its parent index, which captures large, mid and small cap securities. It represents about 99% of the U.S. REIT universe. The index is calculated with dividends reinvested on a daily basis.

The NFI-ODCE is a capitalization-weighted, gross of fees, time-weighted return index with an inception date of December 31, 1977. Published reports also contain equal-weighted and net of fees information. Open-end funds are generally defined as infinite-life vehicles consisting of multiple investors who have the ability to enter or exit the fund on a periodic basis, subject to contribution and/or redemption requests, thereby providing a degree of potential investment liquidity. The term diversified core equity typically reflects lower risk investment strategies utilizing low leverage and is generally represented by equity ownership positions in stable U.S. operating properties diversified across regions and property types. While funds used in the NFI-ODCE have characteristics that differ from BREIT (including differing management fees and leverage), BREIT’s management feels that the NFI-ODCE is an appropriate and accepted index for the purpose of evaluating the total returns of direct real estate funds. Comparisons shown are for illustrative purposes only and do not represent specific investments. Investors cannot invest in this index. BREIT has the ability to utilize higher leverage than is allowed for the funds in the NFI-ODCE, which could increase BREIT’s volatility relative to the index. Additionally, an investment in BREIT is subject to certain fees that are not contemplated in the NFI-ODCE.

The S&P 500 Index is a market capitalization-weighted index that includes 500 stocks representing all major industries. Returns are denominated in U.S. dollars. The S&P 500 Index is a proxy of the performance of the broad U.S. economy through changes in aggregate market value. The S&P 500 Index is a widely used barometer of U.S. stock market performance. The key risk of the S&P 500 Index is the volatility that comes with exposure to the stock market.

Forward-Looking Statement Disclosure

This material contains forward-looking statements within the meaning of the federal securities laws and the Private Securities Litigation Reform Act of 1995. These forward-looking statements can be identified by the use of forward-looking terminology such as “outlook,” “indicator,” “believes,” “expects,” “potential,” “continues,” “identified,” “may,” “will,” “could,” “should,” “seeks,” “approximately,” “predicts,” “intends,” “plans,” “estimates,” “anticipates”, “confident,” “conviction” or other similar words or the negatives thereof. These may include financial estimates and their underlying assumptions, statements about plans, objectives, intentions, and expectations with respect to positioning, including the impact of macroeconomic trends and market forces, future operations, repurchases, acquisitions, future performance and statements regarding identified but not yet closed acquisitions or dispositions and pre-leased but not yet occupied development properties. Such forward-looking statements are inherently subject to various risks and uncertainties. Accordingly, there are or will be important factors that could cause actual outcomes or results to differ materially from those indicated in such statements. We believe these factors include but are not limited to those described under the section entitled “Risk Factors” in BREIT’s prospectus and annual report for the most recent fiscal year, and any such updated factors included in BREIT’s periodic filings with the SEC, which are accessible on the SEC’s website at www.sec.gov. These factors should not be construed as exhaustive and should be read in conjunction with the other cautionary statements that are included in this document (or BREIT’s public filings). Except as otherwise required by federal securities laws, we undertake no obligation to publicly update or revise any forward-looking statements, whether as a result of new information, future developments or otherwise.

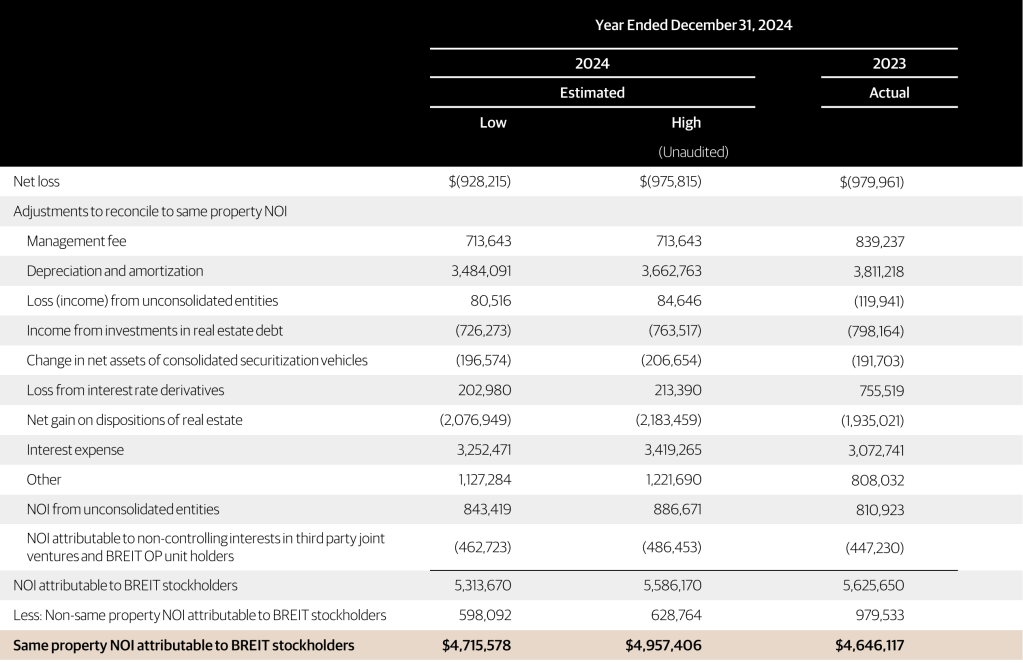

The following table reconciles preliminary estimated GAAP net loss to preliminary estimated same property NOI for the years ended December 31, 2024 and 2023 ($ in thousands). Same property NOI growth is estimated to be 4% year to date based on the midpoint of the estimated year-over-year increase.